Buying car insurance is not only about meeting a legal requirement. It is also about understanding what kind of financial protection stands behind the policy when damage, liability, or repair costs arise. For many vehicle owners comparing car insurance plans, the real question is whether basic legal cover is enough or broader protection makes better sense.

This blog explains what each option is designed to cover and where the difference matters.

What is Third-Party Car Insurance?

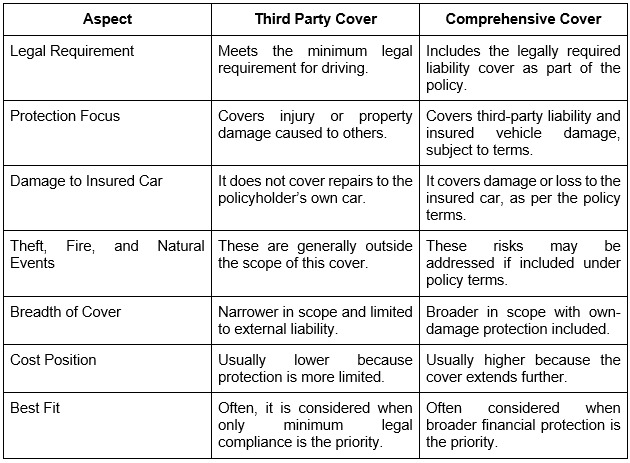

Third party car insurance is the legally required form of cover for driving on public roads in India. It is designed to protect against financial liability when the insured vehicle causes injury or property damage to another person.

The policy is not meant to pay for damage to the insured car itself. In simple terms, it addresses legal and compensation obligations arising from harm caused to others during an accident, rather than covering the policyholder’s own repair expenses.

What is Comprehensive Car Insurance?

Comprehensive car insurance includes third-party liability cover and protection for damage to the insured car, subject to the policy terms. It is designed to support the policyholder not only when another person suffers loss, but also when the insured vehicle is affected by covered events such as accidents, theft, fire, or certain natural causes. In simple terms, it offers wider financial protection than a policy limited only to liability towards others.

Key Differences Between Comprehensive and Third-Party Insurance

Both policies serve different purposes, even though they relate to the same vehicle. The difference becomes clearer when legal cover, vehicle damage, and protection are compared side by side.

Which One Should You Choose?

The choice should be based on risk exposure, vehicle value, usage pattern, and the level of financial protection considered necessary.

Choose Third Party if:

- The main concern is to fulfil the legal requirement for using the vehicle on public roads without extending protection to own damage.

- The car is older, and the owner is willing to manage repair costs if the vehicle is damaged in an accident

- The focus is limited to liability towards another person, including bodily injury or damage to third-party property.

- Budget sensitivity is high, and the aim is compliance rather than broader cover for the insured vehicle.

- The vehicle is used in a way where the owner accepts a narrower level of financial protection.

Choose Comprehensive if:

- The vehicle still holds considerable value, and repair or replacement costs would place pressure on household finances.

- The owner wants protection that addresses liability towards others, as well as covers loss or damage affecting the car.

- The car is used frequently, which can increase exposure to accidents and other insured risks during travel.

- Greater financial protection is preferred over choosing only the minimum level of cover required by law.

- The policy is expected to support wider protection rather than functioning only as a legal necessity.

Conclusion

The difference between these two options comes down to purpose. One is built to comply with a legal duty towards others, while the other is meant to support both liability protection and damage cover for the insured car.

A careful choice depends on the vehicle’s age, everyday use, and the level of financial exposure. Understanding that design helps in choosing a cover with clarity, instead of choosing only by price.