Many first-time homebuyers begin their property search after getting a pre-approval letter from a lender and treat it as a guarantee that the home loan will be sanctioned. This assumption leads to a surprisingly common and painful situation: the buyer finds a property, agrees on a price, pays a booking amount, and then discovers at the final approval stage that the loan may not be disbursed because of issues with the property or a change in the borrower’s financial profile.

Understanding the difference between pre-approval and final approval is important when financing a home purchase. It also helps borrowers know what factors may change between these two stages.

What Pre-Approval Actually Means?

A home loan pre-approval, also called an in-principle approval or sanction letter, is the lender’s conditional commitment to provide a loan of a specified amount, subject to verification of the property and no material change in the borrower’s financial profile before disbursal. The pre-approval is based on the borrower’s income, credit score, and existing obligations as provided at the time of application.

It is an assessment of borrower eligibility, not property eligibility. The lender has confirmed that the borrower looks creditworthy for a certain loan amount. They have not yet evaluated whether the specific property the borrower intends to purchase meets their lending criteria.

What does Final Approval Mean?

Final approval, or the formal sanction, happens after the borrower has identified a specific property and submitted the property documents to the lender. At this stage, the lender commissions an independent legal verification of the property title and a technical assessment of its market value and construction quality.

The loan amount in the final approval is based on the lower of the agreed purchase price and the lender’s assessed market value, applied against the eligible LTV ratio. If the lender’s valuation is lower than the price agreed upon by the buyer and seller, the approved loan amount may be lower than expected, requiring the buyer to make a larger down payment.

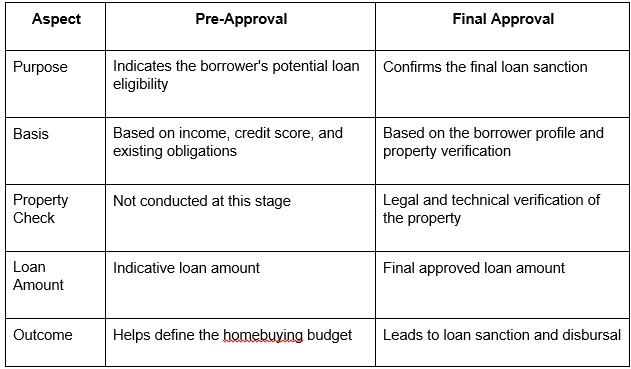

Pre-Approval vs Final Approval: Key Differences

Pre-approval and final approval are two important stages in the home loan process. The following table highlights the main differences between them.

Things That Can Change Between Pre-Approval and Final Approval

Several factors are reviewed in detail between the pre-approval stage and the final home loan approval. Changes or new findings during this stage can influence the lender’s final decision.

1. Property Valuation

The lender conducts an independent valuation of the property. If the assessed value is lower than the agreed purchase price, the eligible loan amount may be reduced.

2. Legal Verification of the Property

During the legal review, the lender examines property documents to confirm clear ownership and compliance. Issues such as title defects, missing ownership records, or existing encumbrances may delay or affect approval.

3. Changes in the Borrower’s Financial Profile

If the borrower changes jobs, experiences a break in employment, or takes on additional credit obligations, the lender may reassess the borrower’s repayment capacity.

4. Changes in Credit Score

A noticeable drop in the CIBIL score, possibly due to missed payments or new credit inquiries, can influence the lender’s risk evaluation.

5. Builder and Project Verification

For under-construction properties, lenders also review the builder’s track record, project approvals, and RERA registration. Any discrepancies in these areas may delay or impact the final approval process.

6. Final Interest Rate Determination

In some cases, the final home loan interest rate may differ slightly from the indicative rate mentioned during pre-approval. Changes in market conditions or the lender’s final assessment of the borrower and property may influence the applicable rate. Borrowers are usually advised to confirm the interest rate at the final sanction stage to understand the expected EMI clearly.

How to Use Pre-Approval Correctly?

A pre-approval letter serves an important and legitimate purpose: it tells the buyer their realistic budget before they begin the property search, and it signals to sellers and brokers that the buyer is a serious, creditworthy party. These benefits are real and make the home purchase process more efficient.

The correct way to use it is as a budget guide and a negotiating tool during the property search, not as a guarantee of final funding. Buyers who understand this distinction protect themselves from overcommitting to a property before the full disbursal conditions are confirmed.

How the Home Loan Process Moves From Pre-Approval to Final Approval

Many lenders structure the home loan journey so that both pre-approval and final approval are handled within a single application process. Borrowers usually begin by submitting income details, credit information, and basic KYC documents to receive a pre-approval that indicates their potential borrowing capacity.

Once the borrower identifies a property, the application progresses to the next stage. The lender then conducts legal verification of property documents and a technical assessment of the property’s value and condition. For example, lenders such as Tata Capital offer home loan processes where pre-approval and final sanction are managed through a streamlined workflow, helping borrowers track their application progress more efficiently.

Conclusion

Pre-approval and final approval are two distinct stages in the home loan journey, each serving a different purpose. While pre-approval helps borrowers understand their potential borrowing capacity, final approval depends on property verification and a detailed review of the borrower’s financial profile. The home loan interest rate and final loan amount may also be confirmed at this stage. Treating pre-approval as a budgeting tool rather than a guaranteed sanction can help buyers make informed decisions and move through the home loan process with greater clarity.