According to the EY report by Rakesh Jariwala, Partner-EY India, following is the impact of Modi Govt’s budget 2020 on the Media and Entertainment industry.

The M&E sector in India is expected to grow at a CAGR of 10-11% till 2025. This impressive growth factors various opportunities for the Indian media businesses both within and outside India, as well as for foreign media businesses in India; with both aiming to make a healthy contribution towards India’s US$ 5 trillion aspiration.

Media businesses globally are very interestingly poised: As the world is become more and more digital, amongst others, technology, telecom, automotive businesses are discovering the power and influence content has over masses and deploying content to peddle their businesses.

The Union Budget 2020 introduced various proposals which have a bearing on the Media & Entertainment industry. On the digital tax front, the G20 and OECD have been working on finalising the report on addressing challenges to tax digital economy transactions by end of 2020.

Key proposals

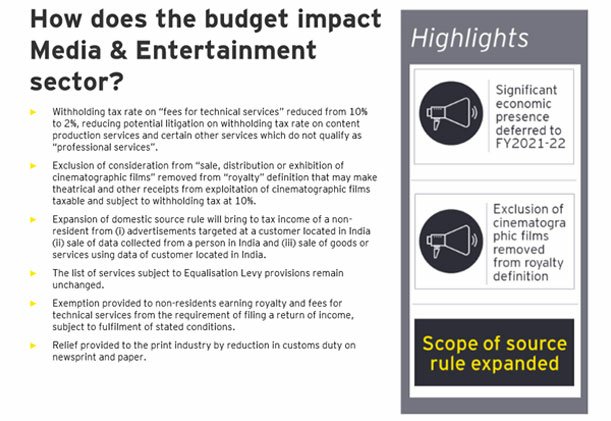

According to Rakesh Jariwala the Definition of “royalty” amended to remove exclusion of “sale, distribution or exhibition of cinematographic films”

Theatrical and other receipts from exploitation of cinematographic films will be subject to tax and/ or withholding tax under the domestic tax law.

Consideration from digital exploitation of content will no longer be able to take shelter under the above exclusion and will be subject to tax and/ or withholding tax under the domestic tax law.

Consequential withholding tax @ 10% may result in working capital challenges for the businesses.

Amendment to apply from 1 April 2020 onwards.

Digital is here!

Jariwala feels Significant Economic Presence provision introduced in the Finance Act 2018 under the scope of “business connection” (i.e. Permanent Establishment provisions under the domestic tax laws) to tax digital economy transactions deferred to 1 April 2021 in light of ongoing G20/ OECD BEPS project

G20/ OECD report expected by the end of December 2020.

Revenue and user thresholds not notified yet.

The list of specified services chargeable to Equalisation Levy remains unchanged. The Government has the power to expand the scope separately through a notification..

Scope of source rule under the domestic tax law in the event of a “business connection” expanded to include income from:

Advertisements targeting an Indian customer or a customer who accesses the advertisement through internet protocol address located in India;

Sale of data collected from an Indian resident or from a person who uses internet protocol address located in India; and

Sale of goods or services using data collected from an Indian resident or from a person who uses internet protocol address located in India.

According to Jariwala Nexus rules using IP address, location of device and other parameters for affixing customer location have been subject matter of extensive debate globally. Practical challenges of making income determination on the defined basis and potential overlaps with Significant Economic Presence provisions will have to be carefully considered. Additionally, compliance requirements such as filing of return of income could also follow.

Foreign businesses operating in new media and digital space which do not have tax treaty protection will be governed by the amended provisions.