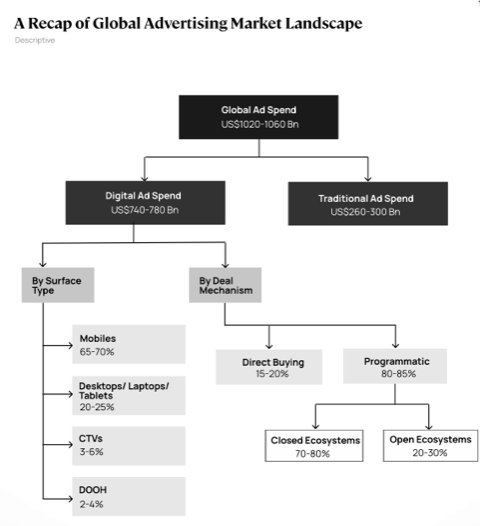

Mumbai: The global advertising industry has entered a defining phase of structural transformation, with total ad spend crossing the $1 trillion mark in 2025, according to the latest report, “Advertising is the Oil Powering the Digital Economy” (April 2026) by Redseer Strategy Consultants. The report underscores a fundamental shift: advertising is no longer just a marketing lever but the core economic engine powering the modern internet.

At the heart of this transformation is digital advertising, which now accounts for nearly three-quarters of global ad expenditure, estimated at $740–780 billion in 2025. This rapid expansion is significantly outpacing global economic growth, with advertising growing nearly three times faster than real GDP. The trend reflects a structural, rather than cyclical, shift in how businesses drive demand and how digital ecosystems monetise user engagement.

Attention is Abundant, But Fragmented

One of the report’s central insights is the paradox of consumer attention. While global internet users—now over 6 billion, or roughly 73% of the population—spend an average of 6.5 hours per day online, their attention is increasingly fragmented across more than 30 apps and multiple devices.

This fragmentation is being accelerated by a surge in app ecosystems, with downloads reaching nearly 280,000 per minute globally. Even within individual categories such as video streaming, households now engage with multiple platforms simultaneously, signaling the end of the “one platform reaches all” era.

For advertisers, this shift has profound implications. Broad reach is becoming commoditised, while precision targeting and contextual relevance are emerging as key competitive advantages.

Digital Advertising Outpaces the Economy

Advertising’s expansion is not just rapid—it is structurally embedded in economic growth. In 2025, global ad spend grew by approximately 9%, compared to 3% real GDP growth. This divergence has pushed advertising intensity (ad spend as a share of GDP) to nearly 0.9% globally, with mature markets like the United States reaching as high as 1.4%.

The growth is being driven by three major forces: deeper digital penetration, the rise of new high-growth channels such as connected TV (CTV) and retail media, and the proliferation of direct-to-consumer (D2C) brands that rely heavily on paid acquisition strategies.

Retail media alone has emerged as a major growth driver, accounting for $170–180 billion in ad spend, while CTV continues to scale rapidly as streaming platforms introduce ad-supported models.

Mobile Leads, In-App Dominates

The report highlights the dominance of mobile as the primary advertising surface, accounting for 65–70% of digital ad spend. Within mobile, in-app advertising commands up to 80–85% share in developed markets, driven by higher engagement and conversion rates that are two to three times higher than mobile web.

Connected TV is also gaining traction, particularly among premium audiences in living-room environments, while traditional desktop usage continues to decline in relative importance.

Geographically, the United States remains the largest digital advertising market, contributing approximately 46% of global spend, followed by China at 24%. Emerging markets such as India, while smaller in absolute terms, are expected to grow at a faster pace of 10–15% CAGR, indicating significant headroom for expansion.

Programmatic Becomes the Default Infrastructure

A defining feature of the modern advertising ecosystem is the dominance of programmatic advertising, which now accounts for over 80% of digital ad spend globally. This automated, data-driven system enables real-time buying and selling of ad inventory, replacing traditional manual processes.

Programmatic platforms process more than 50 trillion ad requests annually, with transactions completed in under 300 milliseconds. This scale and speed have transformed advertising into a high-frequency, algorithm-driven marketplace for consumer attention.

However, the programmatic value chain is complex and layered. Publishers typically capture 45–55% of advertiser spend, while the remainder is distributed across demand-side platforms (DSPs), supply-side platforms (SSPs), exchanges, and agencies.

Walled Gardens Tighten Their Grip

The report points to a growing concentration of power within “walled garden” ecosystems such as Google, Meta, and Amazon. These platforms account for 70–80% of global programmatic ad spend, leveraging their vast first-party data and closed-loop measurement capabilities.

In contrast, the open internet—despite accounting for more than half of total user time—captures only 20–30% of ad spend. This imbalance reflects structural advantages enjoyed by closed ecosystems, including superior targeting precision and operational simplicity.

At the same time, the open ecosystem is undergoing consolidation, with independent adtech players integrating vertically across demand and supply layers to compete more effectively.

AI and Privacy to Reshape the Industry

Looking ahead, Redseer identifies artificial intelligence and privacy regulations as the twin forces that will redefine the advertising landscape.

The decline of third-party cookies and increasing data privacy regulations are forcing a shift toward first-party data strategies, clean rooms, and privacy-preserving targeting methods. Simultaneously, AI is transforming every layer of the advertising stack—from audience targeting and bidding to creative production and campaign optimisation.

Generative AI, in particular, is enabling advertisers to produce large volumes of customised creative assets across formats and languages, dramatically improving efficiency. However, it also introduces new challenges, including sophisticated ad fraud driven by synthetic identities and deepfake content.

A New Playbook for Stakeholders

The report outlines a strategic reset for all stakeholders in the ecosystem:

- Publishers must move beyond scale-driven monetisation and focus on building direct audience relationships and first-party data assets.

- Ad platforms need to invest in AI-driven infrastructure, privacy-first technologies, and transparent measurement systems.

- Advertisers are being urged to strengthen their first-party data capabilities, adopt AI-native campaign execution, and diversify spending beyond dominant platforms.

From Impressions to Outcomes

Perhaps the most significant shift highlighted in the report is the industry’s transition from buying impressions to delivering measurable outcomes. As AI improves targeting accuracy and attribution, advertisers are increasingly prioritising performance metrics such as conversions and return on ad spend (ROAS) over traditional reach-based metrics.

This evolution is expected to reshape value creation across the ecosystem, with platforms competing not just on inventory scale but on intelligence, data quality, and measurable impact.

Redseer’s report positions the advertising industry at a critical inflection point. What began as a tool for brand communication has evolved into the foundational infrastructure of the digital economy.

As consumer attention continues to fragment and technology reshapes the rules of engagement, the winners in this new era will be those who can combine data ownership, AI capabilities, and strategic agility. In this rapidly evolving landscape, advertising is not just fueling the digital economy—it is defining its future.