India’s advertising industry is undergoing a structural transformation, moving beyond a simple shift from traditional to digital media and entering a phase where commerce, content, data and technology are increasingly converged, according to the dentsu Digital Advertising Report 2026.

The report released earlier this year estimates that India’s total advertising spends closed 2025 at Rs. 1.21 lakh crore, growing 8.3% year-on-year, and are projected to reach Rs. 1.40 lakh crore by 2027, translating into a CAGR of over 7%. While this growth appears steady on the surface, the underlying composition of spends reveals a far more consequential change: digital media has become the industry’s primary growth engine and strategic anchor.

Medianews4u.com caught up with Narayan Devanathan, President & Chief Strategy Officer, South Asia, dentsu.

Q. The ad industry is expected to grow by 7.4 percent. How big a threat will things like tariffs, geo political conflict be for the adex to achieve this?

In the short term, businesses will definitely have to contend with the impact of these external factors. However, given India’s focus as an economy is on topline growth (i.e. overall GDP) and not necessarily the bottomline (i.e. per capita income) in the medium term, I don’t expect such factors to drastically alter our growth trajectory overall.

Q. Is lack of measurement for some mediums, walled gardens another challenge for the adex in 2026?

I don’t think so. We still rely on readership and subscribership to invest in print, TV is only now coming of age with Connected TV, and the walled gardens have their own shortcomings because they’re mostly behavioral / attitudinal data and not consumption data but that’s changing with the coming of retail media. DOOH is changing how OOH is measured.

If anything, the need for better measurement needs to be balanced with an acceptance that not everything can or needs to be measured. We are dealing with people and culture and sometimes those can only be measured / evaluated in hindsight when the shifts have occurred en masse.

Q. The RMG ban hit ad spends in 2025. The sports genre heavily relied on it. Which categories are expected to fill the gap in 2026? Will the gap be filled completely?

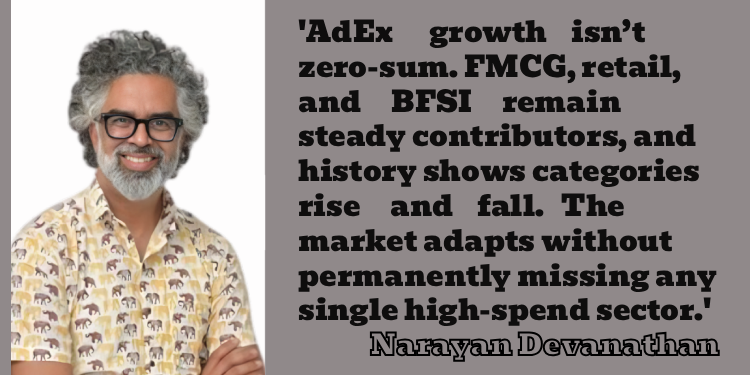

I don’t think this is a zero-sum game. AdEx has been steadily growing and different categories contribute differently over years. While FMCG, retail (including commerce / marketplaces) and BFSI have held steady, other categories have come and gone.

Before RMG, edtech was a huge contributor but we don’t really miss those big spends from them now.

Q. When you talk to clients what is their biggest concern?

It’s probably the scale of fragmentation: of media, customer segments, markets, competition.

Technology is a double-edged sword that makes it easier and more complex at the same time to win and grow today.

Q. Having said all this, is India’s AdEx still in a better state than some other markets like the US since all media including print have growth? In the US print, cable TV are going way.

India has two advantages: The sheer size of the consumer market and the fact that it is still a developing market (in the most positive sense). There’s a lot of headroom for the AdEx to grow in multiple directions, including ones we’ve not yet seen so far.

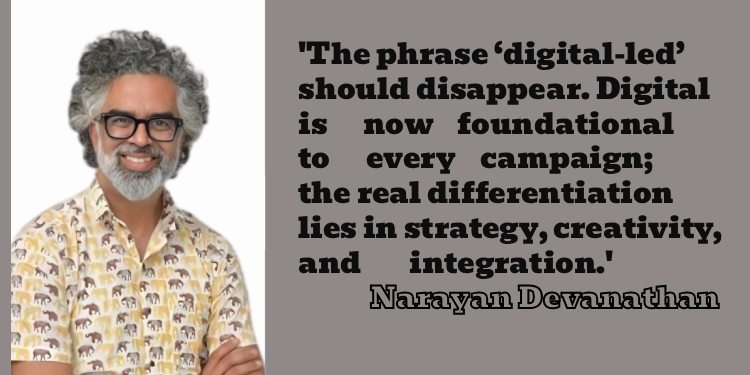

Q. Are we going to see more digital led campaigns in 2026?

I would love to see that phrase becoming extinct in 2026. What’s not digital-led anymore?

Q. How will trends like automation continue to drive programmatic buying in 2026?

The two common factors between automation and programmatic are repeatability and scale. They are made for each other. But the algorithm will have to – very critically – become significantly less error-prone than humans before we can hand over the keys to the machines.

But of all the areas that AI can infuse more efficiency into, this would be among the top.

Q. TV had a difficult 2025. Is 2026 also going to be a struggle?

A couple of interesting things are probably going to shape TV in 2026 especially (and perhaps beyond). The first is the consolidation of the large TV networks with just 3-4 conglomerates, most of which are multi-media groups.

Reliance owns Network18, the Times Group has assets including but beyond TV as does the India Today Group (and I’m only talking about the national networks here). NDTV is perhaps the only one (currently) that isn’t a multi-media group but is still owned by a large conglomerate. But the common thing is that they all can and will likely derive synergy from their respective group’s other businesses (media or non-media).

The second thing is they will likely continue to benefit (like a lot of print media does) from government /political advertising in 2026, especially given it’s an election year in multiple key states. Lastly, CTV will be a space to watch in terms of how TV will adapt and evolve. Competition is coming from non-legacy players like YouTube, Instagram, Samsung, etc.

Q. How is AI going to reshape media buying in 2026?

At dentsu, we talk about brands winning in the Algorithmic Era by maximizing mental availability, physical availability and algorithmic availability. The smarter ways in which AI is able to help strategists navigate the paths to making brands available to customers along these three dimensions, the smarter media buying decisions will become.

While I am tempted to say it will radically reshape media buying from an algorithmic availability perspective alone, I believe the reality is that it will affect all three types of availability. GEO and AEO are only the tips of the iceberg as is AI in programmatic buying.

Q. Is 2026 the year when retail media comes of age due to things like a stronger focus on storytelling? Will it take away digital ad share from Meta, Google?

As I said earlier, because of the nature and lifecycle stage of India as a market, there’s room for everyone and plenty of headroom for growth for everyone.

Retail Media will certainly come of age, and not just because of a stronger focus on storytelling but because it crucially adds the dimension of consumption data on top of behavioural and attitudinal data (the latter two being what Meta and Google are centred around).

Q. We are seeing consumers use LLMs for online product discovery in categories like travel. that is leading to conversions. What opportunities does this provide brands in 2026?

Plan for search and discovery to be optimized by the machine first is my first suggestion to brands. Not because it’s the only or the best option but because it will be an inevitable play to make.

But that also means GEO and AEO will become a level playing field pretty soon and lead to the necessity to find even better ways to connect with humans.

Q. What role will predictive analytics play in helping companies spread spends better during the festive season when everybody will be shouting?

If there’s one predictable thing about people, as the author Dan Ariely famously wrote, it is that we are predictably irrational. With that caveat, I would say predictive analytics can definitely help companies plan festive campaigns and spends better – especially on how much to definitively invest and how much to hedge for unforeseen events impacting things (positively, not just negatively).

I would love for predictive analytics to present a Freakonomics kind of perspective to help identify opportunity beyond the usual.

Q. Microdramas are competing with short form video in terms of consumption. Will brands start exploring the microdrama format in 2026?

Many brands already are and at dentsu we’ve been doing quite a bit of this in stealth mode. Our Dentsu AMP unit was ahead of the curve on this, helping create campaigns using microdramas for Myntra (among others) in 2025 itself, with a whole slate upcoming shortly.

To paraphrase what Howard Gossage said many years back: “People don’t watch ads. They watch what interests them, and currently it’s microdramas.”

Q. Since Gen Z and Gen Alpha value authenticity are they forcing marketers across categories to rewrite the playbook?

This is a deep and interesting question – I want to not accept this notion of these two generations valuing authenticity at face value. Does this mean older generations preferred inauthenticity or didn’t care if brands were authentic or not? I don’t think so.

If anything, we live in a post-truth world now and like so many other things in our lives (identity, profession, sexual preference, relationships), authenticity seems to have become a fluid concept.

I think marketers must rewrite their playbooks, but not only because of this notion about the two most recent generations. A perfect storm ignited by technology, culture and global geo-political connectedness mean new opportunities abound in the here and now. But ultimately, Gen is driven by the same unchanging emotions that have driven humans across time: joy, anger, love, envy, passion, boredom, grief, fear and so on. Before we rush to rewrite playbooks, we should pause to see if our playbooks tell us how to cater to these.

Q. Influencer marketing versus celebrity endorsements. What should brands keep in mind in deciding which direction to take? Influencers are much cheaper.

Here’s the thing about both: if a brand approaches either of them with the firm acknowledgement that brands are about shared meaning, then all that is left is to figure out who can help create and spread that shared meaning about a brand more effectively.

And the answer in most situations is likely to be: it depends. Using celebrity endorsements merely based on their fame is foolish just as it’s stupid to choose influencers based only on their follower count.