A loan against property EMI calculator helps borrowers estimate monthly repayments based on loan amount, interest rate, and tenure. It enables users to compare different borrowing scenarios and understand how changes in these variables affect affordability and total repayment costs. Bajaj Finance Loan Against Property offers funding of up to Rs. 10.50 crore*, interest rates ranging from 8% to 14% p.a., repayment tenures of up to 15 years, and disbursal within 72 hours* of approval, subject to applicable conditions.

Why financial planning matters before taking a loan against property?

A loan against property is often associated with larger loan amounts and longer repayment tenures. While these features provide flexibility, they also create long-term financial commitments. Understanding your future repayment obligations before borrowing can help you avoid financial stress and choose a loan structure that aligns with your goals.

Borrowing beyond eligibility

Many borrowers assume that if they qualify for a certain loan amount, they should borrow the maximum available amount.

- Eligibility differs from affordability: Just because you qualify for a larger loan does not mean it is the right choice.

- Higher borrowing means higher obligations: Larger loans generally lead to bigger EMIs and higher interest costs.

- Future flexibility matters: Borrowing conservatively can leave room for future financial goals.

Understanding your repayment commitments

A loan commitment extends well beyond the approval stage.

- Monthly cash flow impact: EMIs become a recurring financial obligation.

- Long term planning requirement: Repayments may continue for several years.

- Budgeting becomes important: Borrowers need to balance loan repayments with other financial priorities.

What is a loan against property EMI calculator?

A loan against property EMI calculator is an online financial tool that estimates monthly repayments based on three key inputs. The calculator uses information provided by the borrower to estimate the monthly EMI.

- Loan amount: The amount you wish to borrow.

- Interest rate: The applicable borrowing rate.

- Loan tenure: The repayment period selected.

Based on these inputs, the calculator instantly estimates your EMI and helps compare different repayment scenarios.

Why borrowers use it?

An EMI calculator provides much more than a monthly repayment figure.

- Quick comparisons: Compare multiple loan options within minutes.

- Financial visibility: Understand future repayment commitments.

- Informed decisions: Select a loan structure that aligns with your financial goals.

How a loan against property EMI calculator helps with financial planning?

One of the biggest advantages of an EMI calculator is its ability to demonstrate how small changes in loan variables can significantly affect repayments.

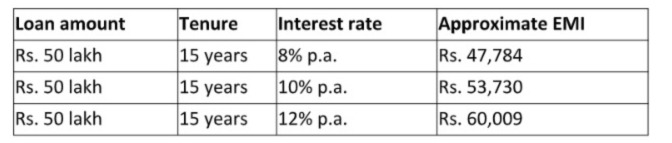

- Understanding the impact of interest rates

Interest rates are among the most important factors affecting borrowing costs. The table below shows how changes in interest rates affect EMI when the loan amount and tenure remain constant.

- Rate sensitivity: Even a small increase in interest rates can significantly affect monthly repayments.

- Borrowing cost visibility: Borrowers can estimate how rates influence total interest outgo.

- Better loan comparisons: Different borrowing options become easier to evaluate.

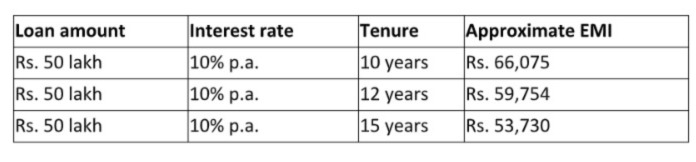

2. Evaluating different repayment tenures

Tenure selection is another important part of financial planning. The table below assumes the same loan amount and interest rate while changing only the tenure.

- Lower EMI versus higher interest: Longer tenures reduce EMI but generally increase total interest paid.

- Cash flow management: Borrowers can select a repayment structure that suits their income.

- Affordability planning: Different tenures support different financial priorities.

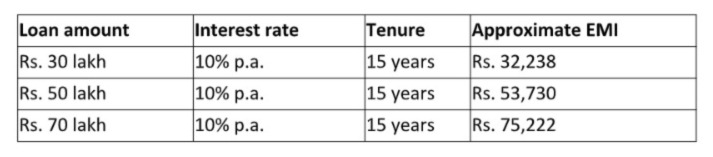

3. Choosing the right loan amount

Many borrowers qualify for more funding than they actually require. The table below illustrates how changing the loan amount affects EMI while keeping the interest rate and tenure constant.

- Right-sized borrowing: Borrowers can align funding with actual requirements.

- Reduced repayment pressure: Smaller loans generally lead to lower EMIs.

- Improved financial balance: Borrowing only what is needed can support long-term financial stability.

Common financial planning mistakes borrowers make

Many borrowers focus solely on loan approval and overlook important repayment

considerations.

1. Looking only at EMI

A lower EMI may appear attractive initially.

- Longer tenure implications: Lower EMIs often result from extended repayment periods.

- Higher overall cost: Total interest outgo may increase significantly.

- Incomplete evaluation: EMI should not be the only factor considered.

2. Ignoring total repayment cost

The total amount repaid is just as important as the monthly EMI.

- Interest accumulation: Longer loans may result in substantial interest payments.

- Long-term affordability: Borrowers should evaluate the complete repayment picture.

- Better decision making: Understanding total costs supports smarter borrowing.

3. Choosing tenure without comparison

Many borrowers select a tenure without evaluating alternatives.

- Missed optimisation opportunities: Another tenure may offer a better balance.

- Cash flow concerns: Poor tenure selection can affect affordability.

- Reduced flexibility: Borrowers may commit to a structure that does not suit their needs.

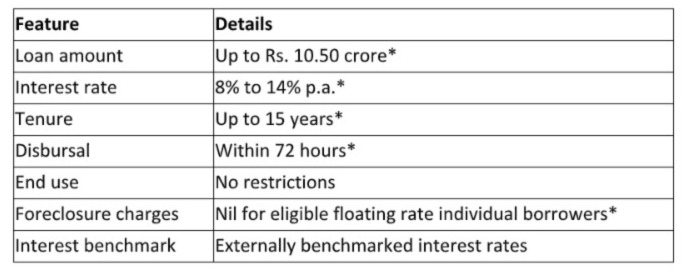

How Bajaj Finance Loan Against Property supports smarter borrowing?

Here are some of the key features of Bajaj Finance that support borrowers looking for a combination of substantial funding, repayment flexibility, and competitive borrowing terms.

Making the most of loan against property EMI calculator

Using an EMI calculator effectively can improve financial planning and borrowing decisions.

4. Compare before you apply

Different loan structures can produce very different outcomes.

- Evaluate multiple scenarios: Compare different rates, tenures, and loan amounts.

- Assess affordability: Understand how repayments fit within your budget.

- Reduce uncertainty: Enter the application process with greater confidence.

5. Review affordability regularly

Financial circumstances can change over time.

- Monitor repayment capacity: Ensure EMIs remain manageable.

- Adjust plans when needed: Revisit assumptions before borrowing.

- Plan responsibly: Maintain financial flexibility for future goals.

6. Align borrowing with future goals

Borrowing decisions should support long-term financial objectives.

- Balance present and future needs: Avoid over-borrowing.

- Protect cash flow: Ensure sufficient room for other commitments.

- Support financial stability: Choose a structure that fits your overall plan.

Conclusion

A loan against property EMI calculator is much more than a repayment estimation tool. It is a financial planning resource that helps borrowers understand the relationship between loan amount, tenure, interest rate, and affordability before making a borrowing decision.

By comparing multiple scenarios, borrowers can evaluate the impact of different interest rates, repayment periods, and funding requirements on their future finances. This allows for better planning, more informed decisions, and greater confidence throughout the borrowing journey.

Bajaj Finance Loan Against Property offers funding of up to Rs. 10.50 crore*, interest rates ranging from 8% to 14% p.a., repayment tenures of up to 15 years, and multiple loan variants to suit different financial needs. When combined with thoughtful planning and effective use of a loan against property EMI calculator, borrowers can create a repayment strategy that supports both immediate funding requirements and long-term financial goals.