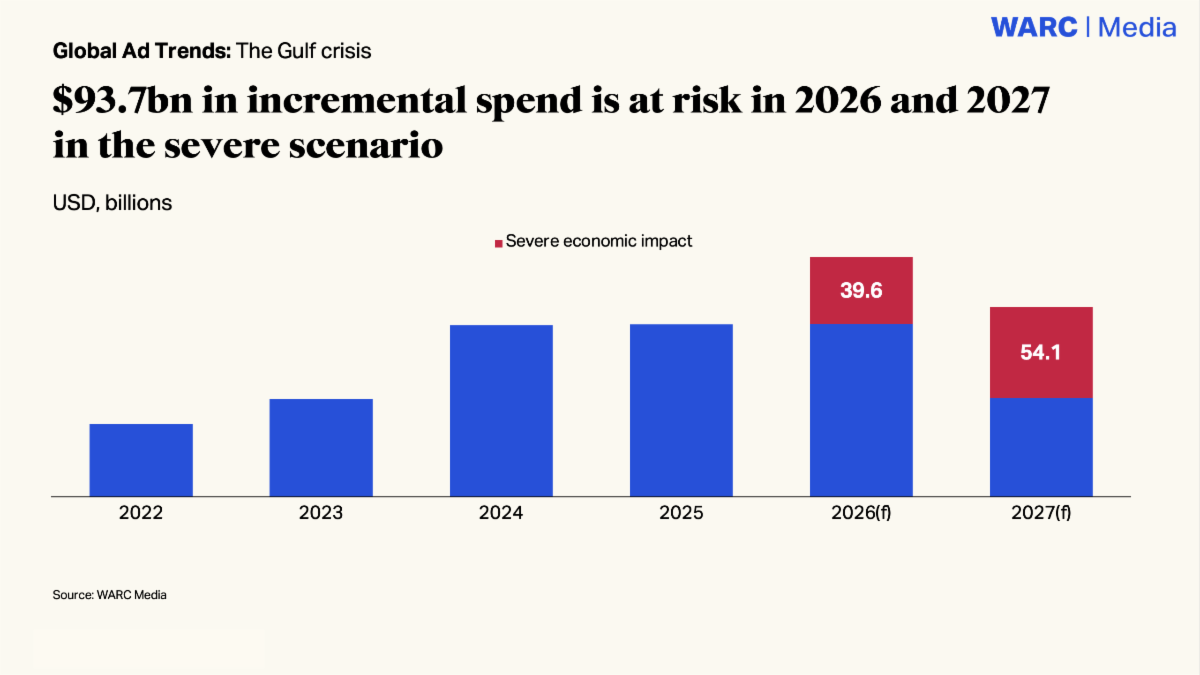

Mumbai: A new outlook from WARC Media has cautioned that the ongoing Gulf Crisis could significantly disrupt global advertising growth, putting an estimated $93.7 billion in incremental ad investment at risk over the next 18 months if the conflict intensifies or continues for a prolonged period.

According to the WARC Media Global Ad Spend Forecast Q2 2026 update: Implications of the Gulf energy crisis, the global advertising market is currently projected to grow 11.5% in 2026 to reach $1.39 trillion, revised upward from the previous 10.6% forecast due to stronger-than-expected momentum from online platforms in the first half of the year.

However, WARC warns that worsening conditions in the Gulf region could reduce growth by as much as 3.2 percentage points, equivalent to $39.6 billion in 2026 alone, with a further $54.1 billion potentially affected in 2027.

Commenting on the findings, James McDonald, Director of Data, Intelligence & Forecasting, WARC, and author of the research, said, “As the Gulf Crisis stretches into its fourth month, global markets are now in damage limitation mode as the blockade of the Strait of Hormuz acts like a tax on consumers, lifting prices and squeezing real spending power.

If the conflict drags on – or further intensifies – these risks shift toward stagflation, with sectors such as travel, automotive, and food acutely exposed to higher production costs and weaker demand. The net effect is a grueling squeeze on margins that could put as much as $94bn of anticipated ad market growth at risk over the coming 18 months.”

WARC’s latest projections are based on advertising investment data aggregated from 100 markets worldwide, supported by a proprietary neural network model using more than two million data points to assess potential outcomes under varying levels of geopolitical severity.

WARC’s latest projections are based on advertising investment data aggregated from 100 markets worldwide, supported by a proprietary neural network model using more than two million data points to assess potential outcomes under varying levels of geopolitical severity.

Regional ad markets expected to experience uneven impact

The study highlights that the effects of the Gulf conflict are likely to vary considerably across regions.

Southeast Asia, projected to grow 6.9% to $24.8 billion in ad spend this year under baseline conditions, is expected to be among the most exposed due to reliance on energy imports and trade routes. Under a severe scenario, growth could slow to 3.6%.

China, where energy imports and shipping costs are creating additional pressure on industrial margins, may see ad growth decline from a projected 7.9% to 5.3%, translating into $5.3 billion in lost growth.

Meanwhile, the United States remains relatively insulated. Even under severe conditions, ad growth is forecast at 7.2%, compared to a baseline estimate of 9.5%, supported by tailwinds including the FIFA World Cup 2026™ and midterm election activity.

Latin America, currently forecast to deliver the strongest regional growth at 12.8%, could see the sharpest downgrade, falling to 3.4% under severe conditions.

The Gulf Cooperation Council (GCC) region faces the most immediate pressure, with WARC projecting advertising investment could contract 0.2% in 2026, compared to baseline growth expectations of 11.7%.

Travel, automotive and food among the most vulnerable sectors

WARC identified travel and transport as the most exposed category, forecasting a 3.5% decline in global ad spend to $34.4 billion this year as airlines reassess budgets amid regional uncertainty.

The automotive sector is also under pressure from rising production costs and weakening consumer demand, particularly in major manufacturing markets such as Germany.

While food advertising is expected to remain resilient in the near term, with projected growth of 10.3% to $99.8 billion, WARC expects supply chain disruptions and input cost increases to have a more pronounced impact through late 2026 and into 2027.

Digital channels remain resilient while traditional media faces pressure

The report also points to diverging fortunes across media channels.

Linear television is expected to face accelerated decline as advertisers prioritise short-term performance channels over traditional brand-building formats. In a severe scenario, linear TV ad spend could decline 7.3% in 2026, compared to a baseline contraction of 3.7%.

By contrast, social media remains relatively resilient, with forecast growth of 20% in the baseline scenario, easing to 17.9% under severe conditions.

Paid search, including generative AI-led formats, emerged as the most stable channel in the outlook, with projected growth of 11% even under severe market conditions.

According to WARC, search, social and retail media are expected to continue accounting for nearly two-thirds of global advertising investment, even in the most disruptive scenarios.

The full WARC Media report will be available to subscribers from 15 June, with a dedicated podcast on the findings scheduled for 18 June.